Multinomial logit¶

Multi-outcome models return one estimate per outcome category. The

session API is unchanged; results carry an outcome axis you can slice

with result.outcome("category").

import numpy as np

import pandas as pd

import statsmodels.formula.api as smf

from pymargins import Margins

rng = np.random.default_rng(3)

n = 4000

df = pd.DataFrame({

"age": rng.integers(18, 70, n),

"income": rng.uniform(20, 200, n),

})

# Three-category outcome: bus / car / bike

util_car = 0.05 * df["age"] + 0.01 * df["income"]

util_bike = 0.02 * (60 - df["age"]) + rng.normal(0, 1, n)

util_bus = np.zeros(n)

util = np.column_stack([util_bus, util_car, util_bike])

util += rng.gumbel(size=util.shape)

df["mode"] = util.argmax(1) # 0=bus, 1=car, 2=bike

# Note: pymargins uses integer outcome indices for MNLogit.

fit = smf.mnlogit("mode ~ age + income", data=df).fit()

Optimization terminated successfully.

Current function value: 0.427064

Iterations 7

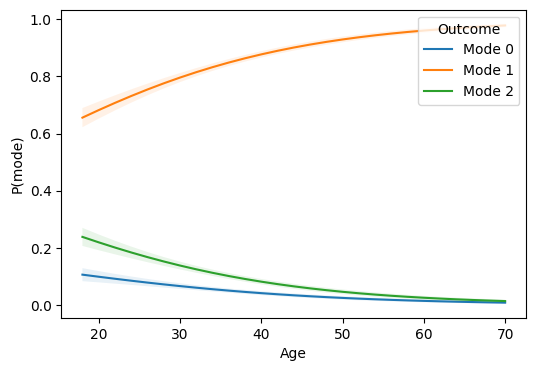

Predicted probability by mode at representative ages¶

m = Margins.linear_scale(fit, at="overall")

preds = m.predict(atexog={"age": [25, 45, 65]})

print(preds.summary())

================================================================

Margins Result (delta, level=0.95)

================================================================

estimate std err z P>|z| [95% Conf. Int.]

----------------------------------------------------------------

age=25 (0) 0.0816 0.0070 11.6543 0.000 0.0679, 0.0954

age=25 (1) 0.7428 0.0111 66.7689 0.000 0.7210, 0.7646

age=25 (2) 0.1756 0.0098 17.9626 0.000 0.1564, 0.1947

age=45 (0) 0.0322 0.0032 9.9477 0.000 0.0258, 0.0385

age=45 (1) 0.9062 0.0053 169.4001 0.000 0.8957, 0.9167

age=45 (2) 0.0616 0.0045 13.7811 0.000 0.0529, 0.0704

age=65 (0) 0.0108 0.0022 4.8803 0.000 0.0065, 0.0152

age=65 (1) 0.9705 0.0036 267.4246 0.000 0.9634, 0.9776

age=65 (2) 0.0186 0.0028 6.5870 0.000 0.0131, 0.0242

================================================================

n = 4000

κ: max=0.202

Delta-vs-sim disagreement: 7.240%

The response scale for multinomial predictions is the probability scale

itself, so linear_scale is the natural default. If you need CIs that

are guaranteed to stay inside [0, 1] for a particular category, you

could open a logit_scale session and then use outcome="car", but

linear_scale is the standard choice for tables and plots.

Plot: predicted probability curves by mode¶

For multinomial predictions the result arrays are 2-D (scenarios × outcomes), so we build the plot DataFrame by hand:

import matplotlib.pyplot as plt

import numpy as np

ages = list(range(18, 71, 2))

res = m.predict(atexog={"age": ages})

est = np.asarray(res.estimate)

se = np.asarray(res.std_error)

ci = np.asarray(res.conf_int())

n_scen, n_out = est.shape

rows = []

for i in range(n_scen):

for j in range(n_out):

rows.append({

"age": ages[i],

"outcome": j,

"estimate": est[i, j],

"ci_lower": ci[0, i, j],

"ci_upper": ci[1, i, j],

})

df_plot = pd.DataFrame(rows)

fig, ax = plt.subplots(figsize=(6, 4))

for outcome, sub in df_plot.groupby("outcome"):

ax.plot(sub["age"], sub["estimate"], label=f"Mode {outcome}")

ax.fill_between(

sub["age"], sub["ci_lower"], sub["ci_upper"], alpha=0.1

)

ax.set(xlabel="Age", ylabel="P(mode)")

ax.legend(title="Outcome", loc="upper right")

<matplotlib.legend.Legend at 0x7f24ccdac350>

AME of income on the probability of car¶

ame = m.dydx("income")

print(ame.outcome(1).summary())

===========================================================

Margins Result (delta, level=0.95)

===========================================================

estimate std err z P>|z| [95% Conf. Int.]

-----------------------------------------------------------

income (1) 0.0009 0.0001 inf 0.000 0.0007, 0.0011

===========================================================

n = 4000

κ: max=0.059

Delta-vs-sim disagreement: 10.667%

Willingness to pay (WTP)¶

In discrete-choice models, WTP for an attribute is the ratio of the attribute slope to the price slope (with a negative sign because price has a negative coefficient):

# Add a price variable to the data for illustration

df["price"] = rng.normal(10, 2, n)

fit_wtp = smf.mnlogit("mode ~ age + income + price", data=df).fit(disp=0)

m_wtp = Margins.linear_scale(fit_wtp, at="overall")

# WTP for one additional unit of income, in price units

wtp = m_wtp.wtp("income", "price")

print(wtp.summary())

/home/hunter/Workspace/pymargins/pymargins/margins/_session.py:972: UserWarning: Delta-method curvature κ=0.582 exceeds threshold (0.3, stacklevel=2); falling back to simulation.

result_data = run_inference(

/home/hunter/Workspace/pymargins/pymargins/margins/_session.py:972: UserWarning: Delta-method curvature κ=0.393 exceeds threshold (0.3, stacklevel=2); falling back to simulation.

result_data = run_inference(

==================================================================

Margins Result (simulation, level=0.95)

==================================================================

estimate std err statistic P>|z| [95% Conf. Int.]

------------------------------------------------------------------

WTP(income) -3.5253 59.9884 -3.5253 0.949 -4.3553, 4.5204

[1] -6.3875 21.1210 -6.3875 0.953 -5.3038, 6.3937

[2] -13.5080 9.5226 -13.5080 0.981 -3.5067, 3.9296

==================================================================

n = 4000

WARNING — Fallback triggered: kappa=0.582>threshold=0.3; kappa=0.393>threshold=0.3

κ: max=0.582

For multi-outcome models, slice to a single alternative first:

wtp_car = m_wtp.dydx("income").outcome(1)

price_car = m_wtp.dydx("price").outcome(1)

from pymargins._result._margins import compose_results

wtp_car_ratio = compose_results(

[wtp_car, price_car],

fn=lambda t: -t[0] / t[1],

label="WTP_car(income)",

)

print(wtp_car_ratio.summary())

/home/hunter/Workspace/pymargins/pymargins/margins/_session.py:972: UserWarning: Delta-method curvature κ=0.582 exceeds threshold (0.3, stacklevel=2); falling back to simulation.

result_data = run_inference(

/home/hunter/Workspace/pymargins/pymargins/margins/_session.py:972: UserWarning: Delta-method curvature κ=0.393 exceeds threshold (0.3, stacklevel=2); falling back to simulation.

result_data = run_inference(

======================================================================

Margins Result (simulation, level=0.95)

======================================================================

estimate std err statistic P>|z| [95% Conf. Int.]

----------------------------------------------------------------------

WTP_car(income) -6.3875 37.3401 -6.3875 0.986 -5.1727, 6.7620

======================================================================

n = 4000

WARNING — Fallback triggered: kappa=0.582>threshold=0.3; kappa=0.393>threshold=0.3

κ: max=0.503